AI is already inside every firm. The harder question for security and compliance leaders is whether they can see what's being used, govern how it's used, and produce a record of it when a client, a court, or a regulator asks.

You Own the AI Risk in Your Bank. Can You See It?

If you run security at a bank, the AI problem has already landed on your desk, whether or not anyone formally put it there. The question that decides how the next year goes is a simple one: can you actually see what AI your people are using, control what data goes into it, and produce a record of it on demand? For most institutions, honestly, the answer is no.

Here are two things that are both true right now. AI adoption across your bank is effectively universal: people in lending, operations, the branch network, and your own team are using it daily. And almost no institution can produce an accurate account of that usage. The exposure lives in the space between those two facts, and it is your space.

The usage you're accountable for is the usage you can't see

The reason this is hard isn't negligence. It's that the AI surface doesn't run through the channels your existing stack was built to watch.

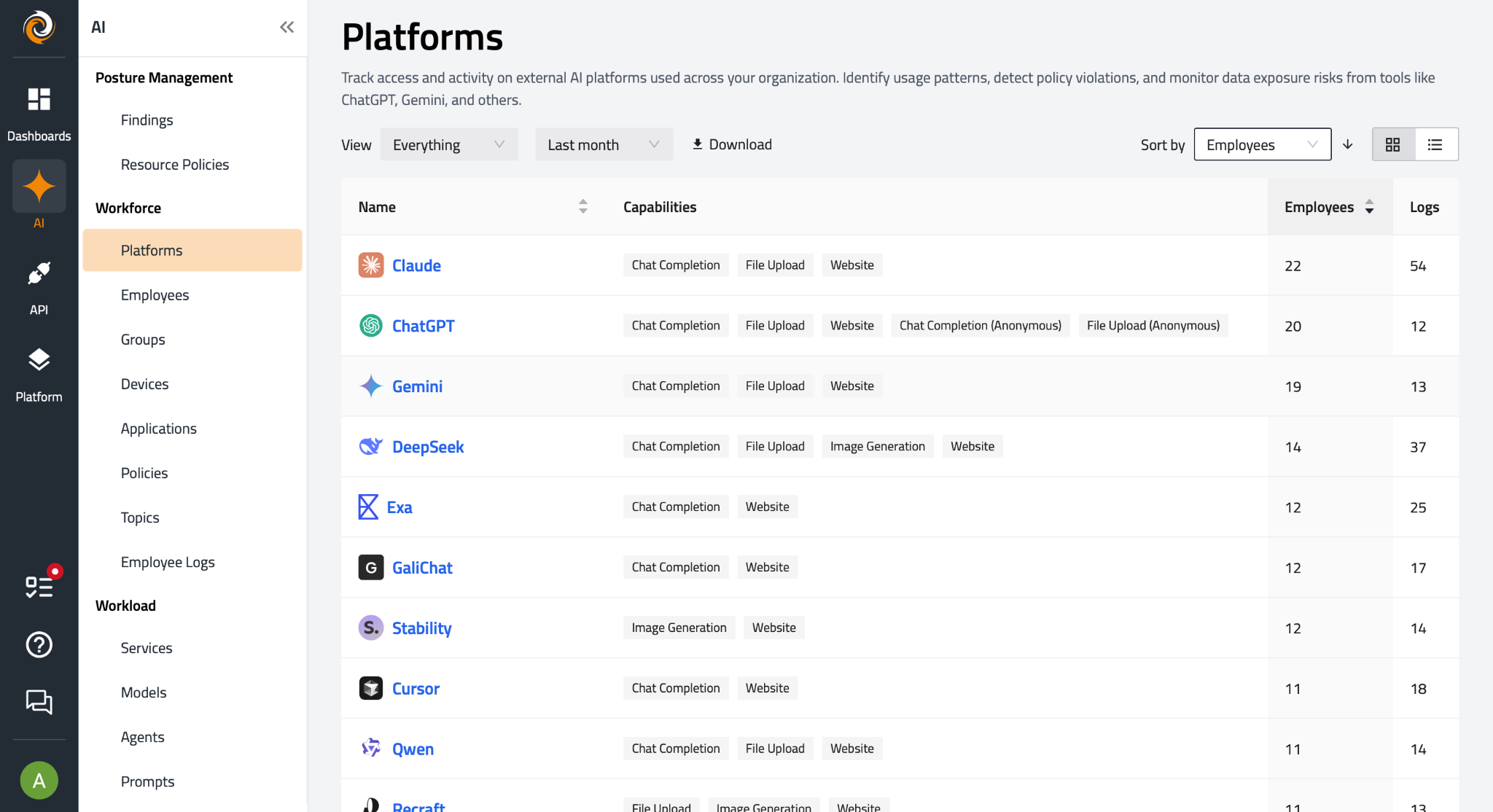

Someone in lending pastes a borrower's financials into ChatGPT to summarise them before a committee meeting. A branch manager drops customer details into a free tool to draft a letter faster. Someone in ops cleans up a spreadsheet full of account numbers in a personal Copilot account. An assistant wired into a core system quietly queries customer records to answer a question no one logged. Your DLP doesn't see most of it, because most of it never touches a channel you control. It's in the browser, on a personal account, inside code, or in an agent acting on its own.

That's the gap. You're accountable for all of it. You can see almost none of it.

What it costs when the gap stays open

In May 2026, a community bank in Pennsylvania showed the industry exactly what this costs.

An employee at Community Bank used an unauthorised AI application to handle non-public customer information: names, Social Security numbers, dates of birth. No attacker, no outage, no financial loss. The bank still determined the event material and filed an 8-K with the SEC, the first ever caused by an employee feeding customer data into an AI tool rather than by a breach.

The filing was the visible part. It was also the least urgent thing that happened. One employee mistake triggered three obligations at once, on three different clocks:

The fastest clock starts the moment you determine an incident happened. Which means the institution that can't see its AI usage is already behind on day one, because it doesn't know the incident occurred until someone outside finds it. The lesson isn't that AI is dangerous. It's that the usage was invisible right up until it became a disclosure.

The risks aren't exotic. They're ordinary uses on a surface you can't see.

None of what happened at Community Bank was sophisticated. It was an ordinary employee, a browser, and customer data, on a channel security wasn't watching. That's the pattern across almost every AI risk that actually matters in a bank.

The ground under your program just shifted

If you were treating AI as something your model risk management program already covered, that assumption stopped holding this year.

On 17 April 2026, the OCC, Federal Reserve, and FDIC issued SR 26-2, replacing the fifteen-year-old SR 11-7 framework with a principles-based approach, and explicitly placing generative and agentic AI outside the old model-risk frame. An AI-specific request for information is expected to follow. The carve-out doesn't mean AI is unregulated. It means the consolidated rulebook your program leaned on no longer answers the question, and the gap lands on you to fill in the meantime.

On 19 February 2026, the Treasury released the Financial Services AI Risk Management Framework, the first federal AI risk resource built specifically for financial services, translating the NIST AI Risk Management Framework into hundreds of control objectives. It's quickly becoming the reference point for what a credible bank AI program looks like.

And the authorities that already applied to AI use still apply with full force: the Gramm-Leach-Bliley Act and interagency guidance on customer data, third-party risk guidance (your bank owns the risk from any AI tool its people use, approved or not), fair-lending and adverse-action rules where AI touches credit, and Regulation S-P. For credit unions, the NCUA carries the same expectations. The direction across all of it points at one capability: being able to show what AI is in use and how it's controlled. That capability is a security problem before it's a compliance one, which is why it sits with you.

Closing the gap: what it actually takes

The questions you're being asked are use cases, not features. Here's how FireTail maps to them.

See every AI tool, model, and agent in use, before anyone asks. Continuous discovery surfaces AI usage across browsers, endpoints, cloud, and code, including the personal-account usage that never touches a monitored channel. The inventory you can't produce by hand exists and stays current.

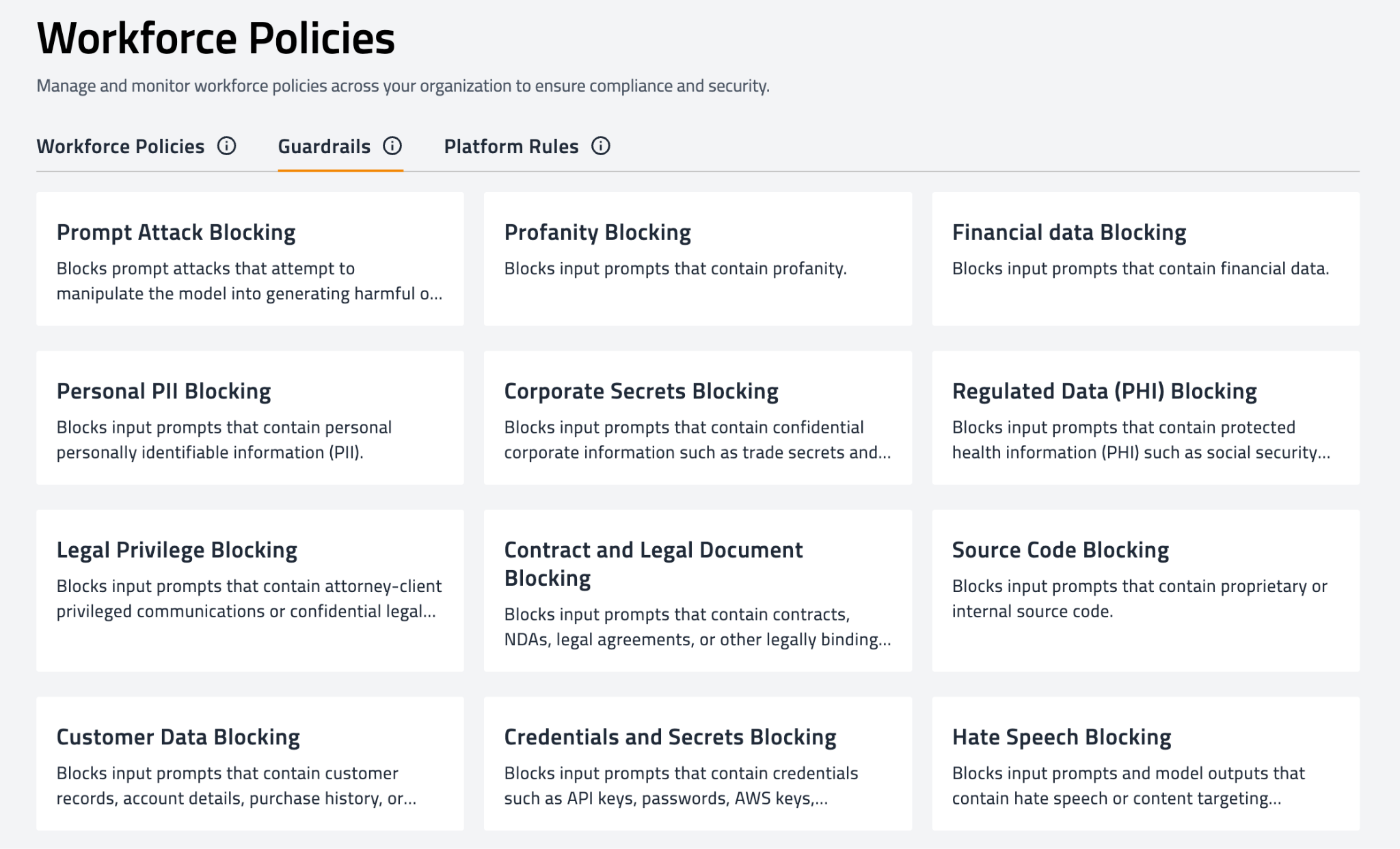

Stop customer data before it reaches a public model. FireTail inspects prompts as they're entered, detects non-public personal information and account data in real time, and applies policy at the prompt itself, with System Guardrails to block, redact, or alert. The employee keeps working. The customer data stays inside the bank.

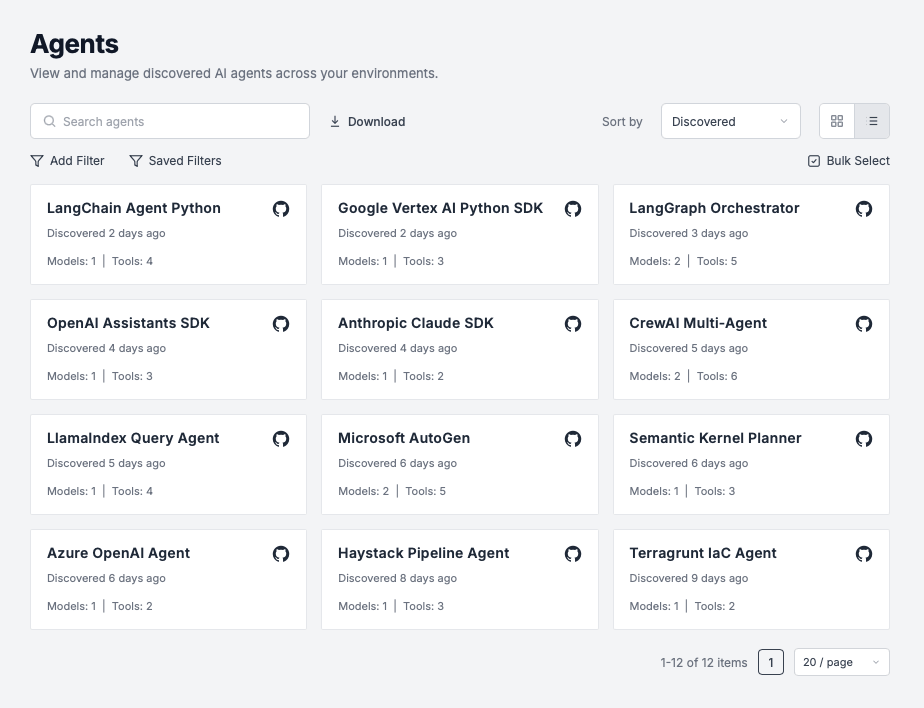

Govern the agents wired into core systems. Discover AI agents and the MCP servers connecting them to internal systems, and govern what they can reach, do, and produce, with the audit trail you need for activity no human directly initiated.

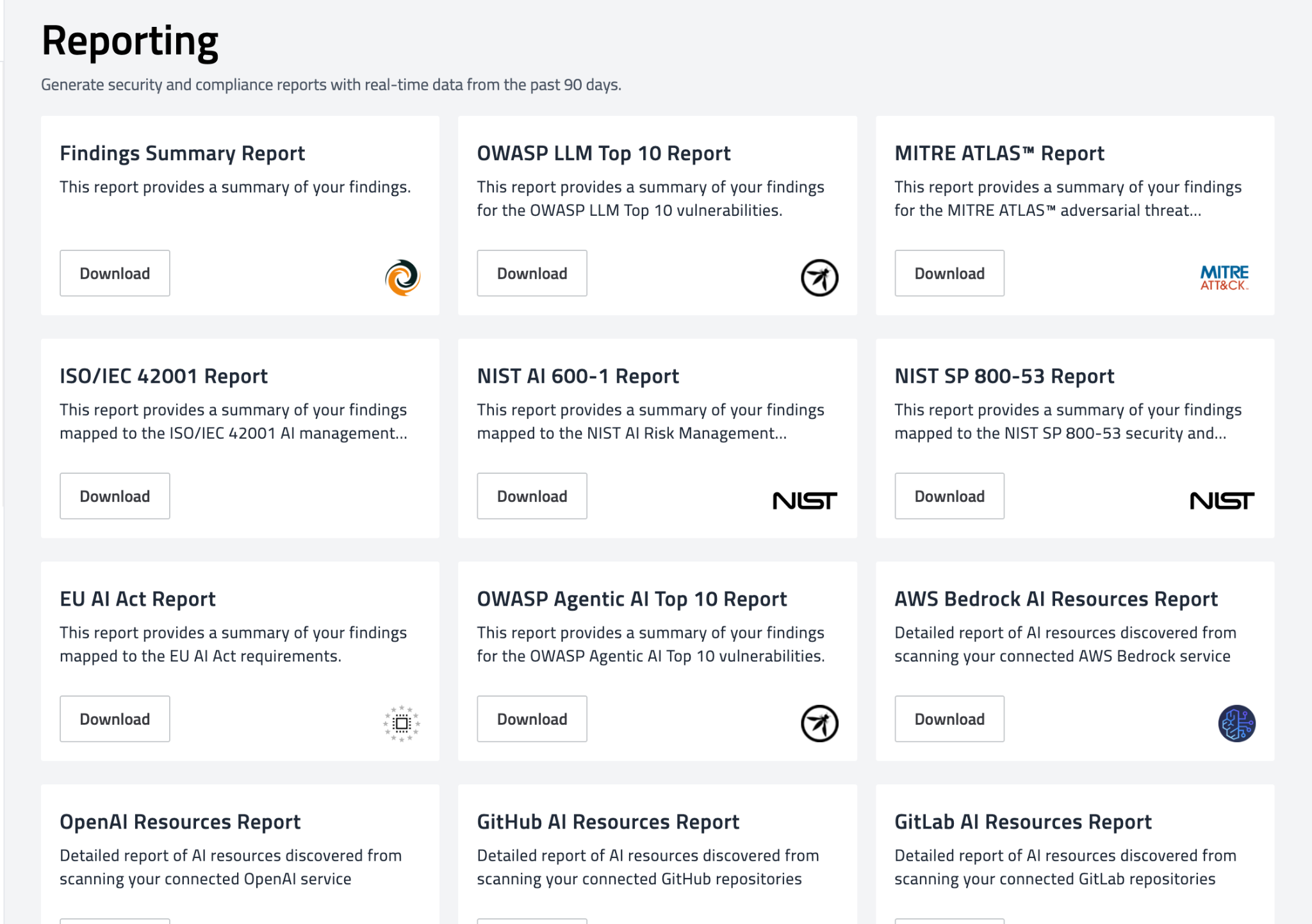

Produce the evidence on demand. Every AI interaction, policy decision, and finding is logged centrally and maps to the frameworks now shaping financial-services AI oversight, including the NIST AI RMF that underpins the Treasury framework, ISO/IEC 42001, and OWASP's LLM and Agentic AI Top 10. When a clock starts or the board asks whether Community Bank could happen here, you have a record, not an intention.

Approve specific tools for specific teams, and apply different policies to lending, operations, and the branch network based on the data each handles. The productivity your people are already reaching for, with controls underneath it instead of a blanket ban they'll route around.

Enable AI instead of banning it.

You can't block your way out of this. The workforce has already adopted AI, and blocking only pushes it onto personal accounts you can see even less of. And you can't policy your way out of it either: a document doesn't tell you what's running right now.

What closes the gap between what you're accountable for and what you can see is visibility, control, and evidence over the actual AI usage in your institution. That's the problem FireTail was built for.

If you want to see what it surfaces in an environment like yours, book a call.